Student Debt Relief: Forgiveness is Just One Piece of the Pie

One in seven Americans has student loan debt, and over 90% of that debt is held by the federal government. This made the White House’s recent reforms to its student loans impactful for roughly ten percent of the population. It is important to note that these changes only apply to federal borrowers, and not to privately held loans. Although most headlines focused on top-line forgiveness, many borrowers will experience far more impactful results based on other changes.

As we review the takeaways, we invite you to forward this information to friends and family who may be affected. And as always, we have compiled this based on the latest public statements, but things may change in the future.

First things first: the freeze on federal student loan payments has been extended for the last time and will end on December 31st. We encourage all borrowers to log into their servicer’s website prior to the end of the year to ensure their contact and payment information remains up to date. You can log into StudentAid.gov to find your loans if your servicer has changed. Many servicers’ websites have been down or laggy in recent weeks because of extra logins due to the changes, but if you can’t get in, set a reminder to check again next week!

Eligibility and Applying for Forgiveness

$10,000 of student loans will be forgiven for eligible borrowers, and for those who received a Pell Grant that goes up to $20,000 – even if your Pell Grant was less than $10,000. This includes Parent Plus loans as well as graduate school loans. The top-line loan forgiveness will apply to single filers with AGI up to $125,000 and married couples or heads of household with AGI up to $250,000. Remember that your AGI is different than your W2 income and includes deductions, so you can check Line 11 of your 2020 and 2021 tax returns to determine where you fall. You can meet the income requirement in either year. Applications will open in October 2022 and be accepted through the end of next year.

Click here to subscribe to be notified when applications open. Check the “NEW!! Federal Student Loan Borrower Updates” box.

If you believe you are eligible and you’re on an income-based repayment plan, you should be automatically granted forgiveness, but just to be sure, you should plan to apply anyway. If you aren’t on an income-based repayment plan, you will need to apply from scratch. The expected timeline for forgiveness to be applied is 4-6 weeks after an application is submitted. If it’s important to you to get it applied before payments start again, plan to apply no later than mid-November.

If your current loan balance is less than the maximum you’re eligible for, you won’t get extra money back. However, if you were making payments during the forbearance period (starting March 2020) that brought your balance below what you’re eligible for, you can request a refund from your servicer. Each servicer’s process is different – we encourage you to make the call and get that figured out ahead of forgiveness being applied!

New Rules for Student Loan Payments

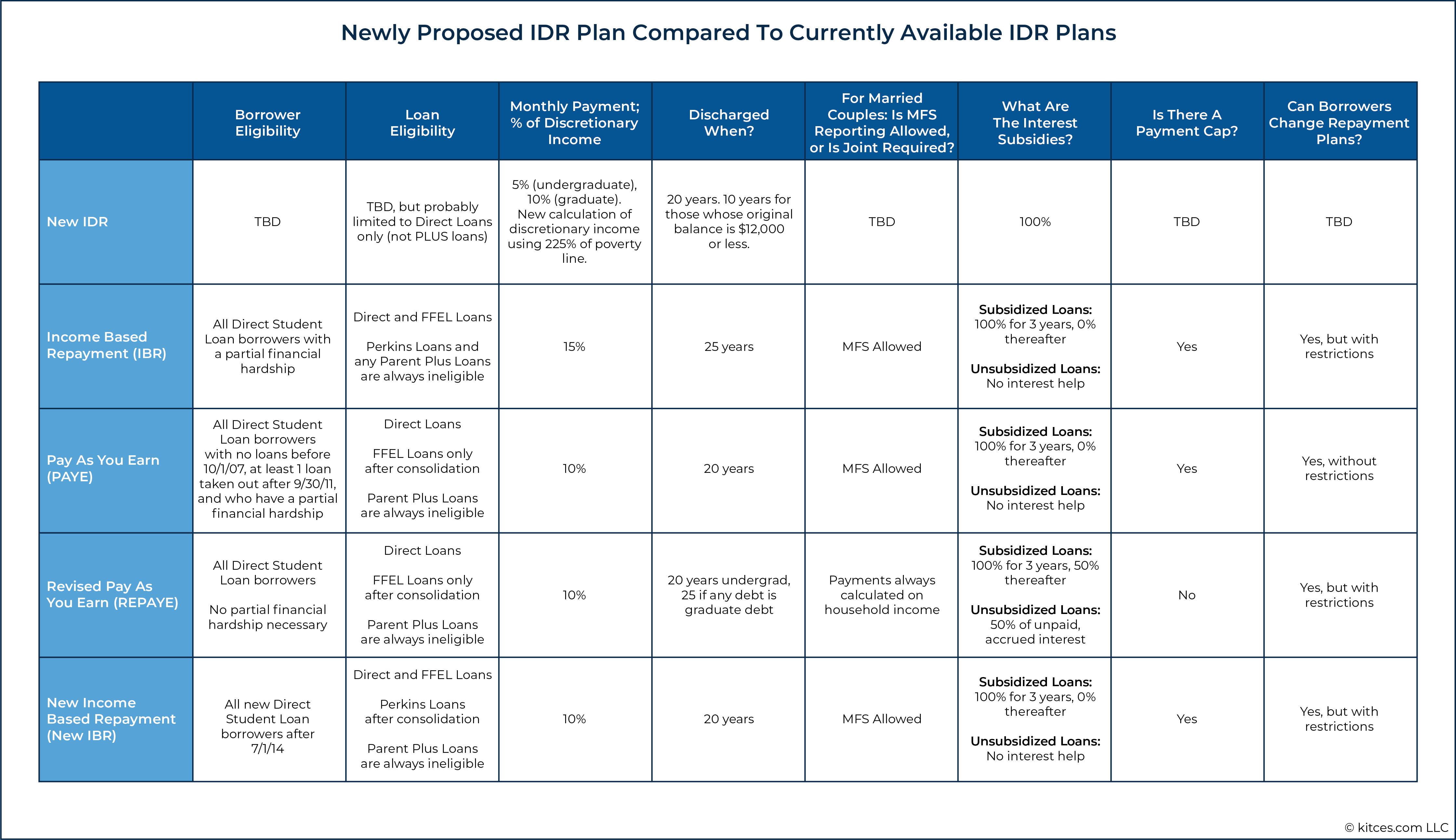

A new Income-Driven Repayment plan (“New IDR”) has been proposed and should go into effect in July 2023. The big changes within this plan are:

A lower cap of monthly income: borrowers will be required to pay only 5% of discretionary income toward undergraduate loans and 10% toward graduate loans, weighted between the two. This is less than current available plans.

Discretionary income is calculated differently in this plan by excluding more income as non-discretionary based on the poverty income guideline (225% instead of 150%).

Under this plan, unpaid monthly interest would be fully covered. Even if your new lower monthly payments wouldn’t cover accrued loan interest, it would be subsidized to prevent your loan balance from increasing (“negative amortization”). This has been a huge problem in past IDR plans, as over 75% of borrowers who enrolled in IDR plans in 2010 owed more in 2017 than they originally borrowed.

Remaining balances will be discharged after 20 years of qualifying payments.

The chart below from Kitces reviews the different available programs, with new IDR at the bottom:

{kind=link}

Changes to Public Service Loan Forgiveness (PSLF)

Borrowers hoping to use Public Service Loan Forgiveness have been flummoxed over the past decade by confusing rules and misinformation that led to hundreds of thousands of rejections for minor errors. In October 2021, the Department of Education created a year-long waiver window for federal borrowers to retroactively apply payments toward their PSLF. That window comes to an end on October 31st of this year, and while a number of these provisions will be included in the reformed PSLF guidelines, we encourage anyone who is planning to use PSLF to ensure their payments have been credited properly and fix any that aren’t.

Click here to access the StudentAid.gov website to determine if the PSLF waiver may affect you.

If you made payments on your loans during forbearance but have been planning to use PSLF, we recommend getting a refund of those payments. The CARES Act of 2020 counts the past two years of forbearance as qualifying payments for PSLF purposes even if you didn’t pay anything.

With any questions regarding applicability of student loans for a loved one, please feel free to reach out to me. We are also proud to share that our associate advisor Patrick Yaghoobians, CFP® will be able to offer limited pro bono student loan planning engagements for non-clients. If you’re not a part of the Horst & Graben family and reading this email has left you overwhelmed and confused about what may apply to you, click here to get in touch with him.